Contributed by: Clare Lilek

Each September, as school is back in session and fall is right around the corner, the last thing on your mind is “How can I make the most of my employee benefit enrollment that’s happening soon?!” It may not be the most exciting topic, but enrollment for your employer’s benefit package happens once a year, usually in late September and early October, and can affect the benefits and coverage you receive for the following twelve months. So it is very much worth your time to look at what your company offers and weigh the pros and cons of all your options. Luckily for you, Nick Defenthaler, CFP®, recently hosted a webinar that outlines the various benefits your company could offer and how you may go about electing certain packages. Below are a few highlights from the 30-minute webinar. For a more detailed explanation, watch the full webinar recording below!

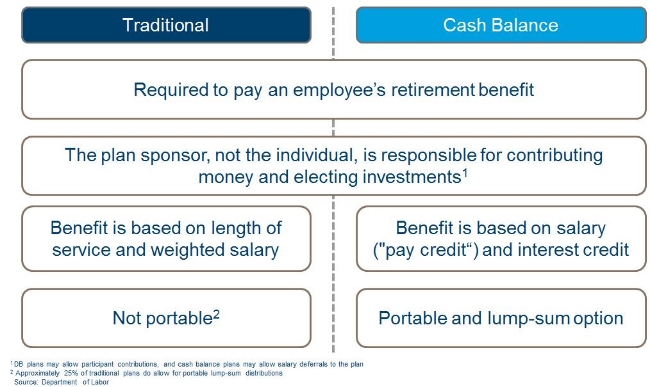

Retirement Savings Plans

Choosing a Traditional (pre-tax) or a Roth (post-tax) plan depends on your current tax bracket versus your projected tax bracket when you retire.

Make sure you are always maxing out your employer match at the very least. In order to make sure you are continually growing your retirement account, consider add 1-2% each year to your contributions.

Choose a mix of investment options that are aligned with your risk tolerance.

Ride out the changes in the market. It’s important not to make constant portfolio changes.

Executive Compensation Plans

These types of compensation plans are typically used as incentive compensation. They can vary from company to company but some of the options include: stock options, non-qualified deferred compensation plans, and employee stock purchase plans. We are currently doing a blog series on Stock Options (NSOs, ISOs, and RSUs); make sure to look out for these for a more detailed overview.

Health Insurance

Nick did a high-level overview of the different types of plans and options you may encounter when it comes to company health insurance. When choosing between a PPO or HMO, you could be choosing between the flexibility of additional benefits (PPO) or the lower cost for potentially more restrictive benefits (HMO). He also highlights the importance of reading the fine print when adding a spouse to your benefits. Lately, many companies have a spousal surcharge that makes it more expensive for a spouse to be insured on your plan if they have access to insurance through their own employer. Nick also noted that some companies are making the move to high-deductible plans, which lower their premiums but put the “buying power” back in the hands of the insured.

Flex Spending Accounts

Nick continued to describe the potential benefit of using a Flex Spending Accounts, whether it’s for medical or dependent care deductibles. When pretax contributions are used for qualified medical expenses, within the year of contribution, they continue to go untaxed. To learn how you could potentially save some tax money, make sure to tune in to this part of the webinar!

Other Insurances

To wrap up, Nick went through disability insurance and life insurance options. He weighed the pros and cons for group vs individual coverage, and how some employees might want to consider long-term and short-term disability coverage.

If you have any questions about this webinar or your specific benefits, don’t hesitate to reach out to Nick.