Stock returns as measured by the S&P 500 were in the hole for the quarter coming into June. They rallied somewhat for the month so that those invested accordingly had the potential to recover some. This time of year also marks some of our most intense research activities including the Morningstar Investment Conference. I summed up our thoughts on portfolio positioning and the Eurozone in a special June update so I'd like to discuss some new trends and themes today.

A laundry list of news items are catching our attention today. They converge to create a growing tally of changes at the margin which may have investment implications for you.

-

We've sent you several communications about the changes to General Motors and Ford pensions. Even if you are not directly impacted, there may see similar changes if you have a defined benefit plan. Analysts believe that this is the start of a new wave of offloading pension obligations and that more announcements from other companies may follow. Our experiences show that the decisions to take a pension or lump-sum buyouts is largely personal and complex based upon your overall financial situation.

- Around the world, interest rates have been falling as slowing growth in China and EuroCrisis have been answered by government intervention. This may be one of the reasons that the MSCI EAFE is flat on the year in spite of dire headlines overseas. While interest rates would be challenged to go lower in the US, there is some room for government intervention around the world, especially in emerging markets -- think of Brazil as an example.

-

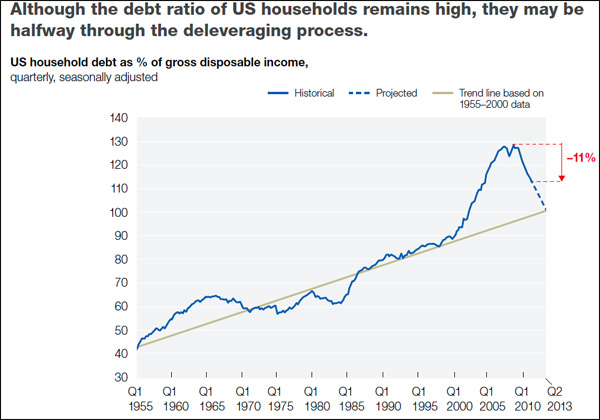

A surprising slowdown in overall US debt growth has been occurring under our nose. No, the US federal debt load keeps growing, but there has been measurable deleveraging on the state and household levels. Some of this has come through the painful process of personal bankruptcy and foreclosures. States and municipalities have been practicing their own austerity with layoffs and less borrowing.

- The Affordable Care Act was largely upheld by the Supreme Court last month. This will have implications for Americans of all walks of life. For some of you some of the implications will be investment-related due to the 3.8% surtax on investment income in higher earnings brackets. This increase on investment income may not be the end given the pending expiration of "Bush" tax cuts. The coordination between tax strategy and investment management will become more and more critical in coming years.

-

Scandalous headlines resurfaced at big banks, most recently JP Morgan and Barclays. JPM disclosed that it had major losses due to poor risk controls in exotic trades. The Barclay's LIBOR scandal is in its early days and may be much larger than it appears on the surface. Essentially, Barclay's has admitted that it fudged reports of borrowing costs over the last five years. Many Americans may have been negatively impacted since adjustable loans linked to LIBOR are widespread for mortgages, student loans, and car loans.

We live in a heavily regulated financial world. I know this as much as anyone as each of these messages to you is reviewed in-depth by a compliance department prior to publishing. If I had my druthers, my day would involve less red tape and easier direct communication with you. The continued misbehavior of corporations and individuals alike seems to justify at least some of this burdensome regulation.

As the election season heats up, Angie Palacios, CFP®, Portfolio Coordinator, has focused her MoneyCentered blog posts on politics and investing. Click here to read the series.

Speaking of politics, I recently heard Columbia University Professor of History Eric Foner in an interview discussing Abraham Lincoln's presidency and leadership strengths. He mentioned that one of Lincoln’s strongest character traits was the ability to change his mind on critical issues. “Lincoln was a flip-flopper, if you want to use the terminology of modern politics.” While a politician today is accused of something close to political treason each time they tweak or change their mind, I value the ability to keep an open mind as an investor.

We think long and hard about what would be best for you as our clients and what worked yesterday may not always work tomorrow. We take the changing investment landscape into consideration as we make investment decisions while we will stick with our process which encourages us to analyze and evaluate risks and opportunities for you. Perhaps if our elected officials were afforded the same flexibility there would be more compromise and less frustration with our nation’s capital.

I always enjoy hearing from those of you who are reading these investment updates. Don't hesitate to let me know if you have any questions, comments, or suggestions for future topics.

On behalf of everyone here at The Center,

Melissa Joy, CFP®

Partner, Director of Investments

Investment Advisor Representative, RJFS

The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Melissa Joy, CFP® and not necessarily those of RJFS or Raymond James. Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users.