With market volatility back, we came together to discuss what occurred in 2018 (particularly in the last quarter) and what we are thinking about for 2019. If you weren’t able to attend, don’t sweat it, we have the cliff notes for you!

On February 27th, 2019, Angela Palacios CFP®, AIF®, Director of Investments, CERTIFIED FINANCIAL PLANNER™, Nick Defenthaler CFP®, Senior Financial Planner, CERTIFIED FINANCIAL PLANNER ™, and Nick Boguth, Investment Research Associate teamed up to tackle these pressing questions and more.

Here is a recap of key points from the “2019 Investment Update”:

What spooked the markets last year:

Decelerating global growth lead by China

Declining earnings growth expectations

Higher short term interest rates in the U.S. and other parts of the world

Valuations started 2018 in elevated territory

UK BREXIT

Italian debt concerns

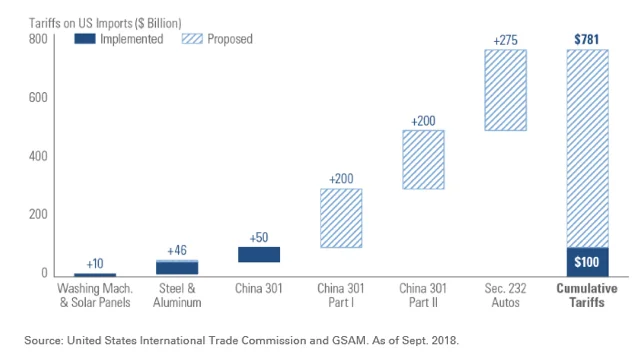

Trade issues

Government shutdown

Mueller investigation

What worked last year:

High quality fixed income rallied in this market

Bond duration – the more the better

Defensive & Low volatility stocks held up better than broad markets

Dividend paying stocks held up better than non-dividend paying stocks

Large cap equities held up better than small cap equities

In the last quarter of 2018 emerging and international developed markets held up better

Is a recession on the horizon: Recessions are mainly caused by four reasons throughout the world (Inflation, Reduction in exports, Financial Imbalance or commodity price crash). Currently inflation is benign here in the U.S., exports are healthy, financial excesses aren’t present (equity valuations and household debt are moderate), and our economy is highly driven by commodities. So at this point it looks unlikely in the next year.

Yield curve: Flattened dramatically last year while the 2 and 5 year treasury bond yields did invert. A traditional inversion is between the 2 and 10 year and is the signal usually watched for to telegraph a coming recession. We are keeping a close eye on this as this is becoming a potential concern.

Tax reform recap: Nick Defenthaler gave us an update on tax reform looking at the changes to income tax brackets, changes in the standard deduction and deductibility of state and local income taxes. If you’d like to hear more on this please listen in on our Year-end tax planning webinar for the details!

Client Portal: A Center for Financial Planning, Inc.® app??!!! We hope you are as excited as we are! Nick Boguth gave a quick demo of our new client portal and document vault. If you are interested in learning more or want to sign up for this service just reach out to your planner!

Angela Palacios, CFP®, AIF® is a partner and Director of Investments at Center for Financial Planning, Inc.® Angela specializes in Investment and Macro economic research. She is a frequent contributor The Center blog.