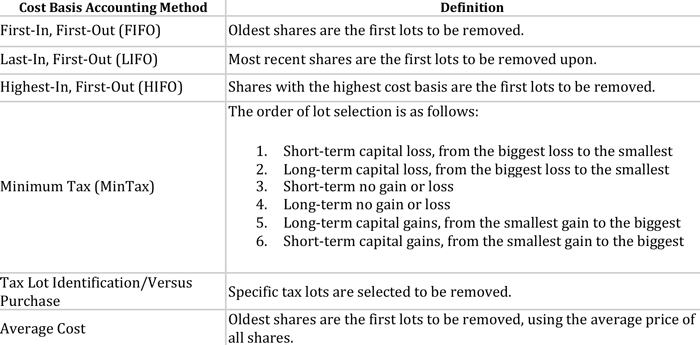

Contributed by: Jaclyn Jackson

By appealing to white, blue collar voters, Donald Trump unexpectedly captured rustbelt states and secured the 2016 presidential election. Additionally, Republicans made a clean sweep taking both the House and Senate majority. Uncertainty remains as many await cabinet selections and the unveiling of comprehensive policy. Market industry professionals anticipate rising performance from equity sectors that benefit from tax reform, infrastructure stimulus, and deregulation. The “Post-Election Day Winners and Losers” chart gives us insight as to how market sectors have performed post-election. Below, I’ve explored how each sector could continue to win or lose under the Trump administration.

The Winners

Industrials/Materials: Throughout the campaign trail, Trump showed great enthusiasm for infrastructure spending. Accordingly, industrials picked up after the election. Civil infrastructure companies and military contractors will likely have more opportunity for government work under his administration. As a result, the material and industrial sectors should have legs to run.

Energy: Companies linked to fossil fuel energy may see a lift under a Republican White House because of less regulation and slower adaptation to renewable energy. Trump’s support of coal energy positions the energy sector for rebound.

Healthcare: Assuredly, the Affordable Care Act is on the agenda for repeal under the Trump administration. Companies that have benefited from Obamacare may decline. In contrast, pharmaceutical and biotech stocks have rallied due to the President-elect’s relatively lenient stance on drug pricing. Yet, there are no sure signs this sector will remain a winner since Trump also favored prescription drugs importation (unconventional for GOP policy) during his campaign run. According to Morgan Stanley analysis, prescription drug importation could negatively impact pharmaceutical companies.

Financials: Banks have rallied as Trump’s victory points towards deregulating financials. Conversely, well-known investment management corporation, BlackRock, challenged that repealing the Dodd-Frank law may result in “simpler and blunter, but equally onerous rules.”

The Losers

Treasuries: As votes tallied in favor of Trump’s victory on election night, investors fled from equities to Treasuries. The risk-off approach, however, dissipated overnight; perhaps because Trump’s victory speech was more conciliatory than expected revealing hope for moderate governance. Ultimately, U.S. Treasury concerns hinge on whether Trump’s policies widen the deficit.

Emerging Markets: Mexico’s reliance on exports to the US leave it vulnerable to tariffs/trade wars, therefore, Mexico and countries alike (Brazil, Argentina, Columbia) could sell off. We’ve already witnessed the peso falling in response to Trump’s protectionist views. On the other hand, JPMorgan’s chief global strategist, Dr. David Kelly, encouraged investors to evaluate emerging markets by their own “strengths.” China and some countries in Latin America, for example, are adjusting well to growth and lack populous sentiment. Overall, emerging markets have forward momentum with improving economies, easing monetary policies, and a global focus on spending.

Developed Markets/Euro: Companies with money overseas in the technology, healthcare, industrials, and consumer discretionary sectors, could gain from Trump’s desire to incentivize business repatriation of offshore cash. Subsequently, the Euro has fallen provided high concentrations of US based multinationals’ earnings are in Europe.

Consumer Stocks: Consumer stocks could be hurt because tougher immigration restrictions may deter labor supply and consumer demand. Additionally, policies that force tariffs on countries like China and Mexico may unintentionally pass on the costs of tariffs to US consumers.

If you have questions about your portfolio or how these “winners and losers” might affect you and your future, please reach out to your planner. We’re always here to help and answer your questions!

Jaclyn Jackson is an Investment Research Associate at Center for Financial Planning, Inc.® and an Investment Representative with Raymond James Financial Services.

The information contained in this blog does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Jaclyn Jackson and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss regardless of strategy selected. This material is being provided for information purposes only and is not a complete description, nor is it a recommendation. This information is not intended as a solicitation or an offer to buy or sell any security referred to herein. Investments mentioned may not be suitable for all investors. Sector investments are companies engaged in business related to a specific sector. They are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification. Investing in emerging markets can be riskier than investing in well-established foreign markets. Investing involves risk and investors may incur a profit or a loss. Past performance may not be indicative of future results.