Contributed by: Angela Palacios, CFP®, AIF®

Contributed by: Angela Palacios, CFP®, AIF®

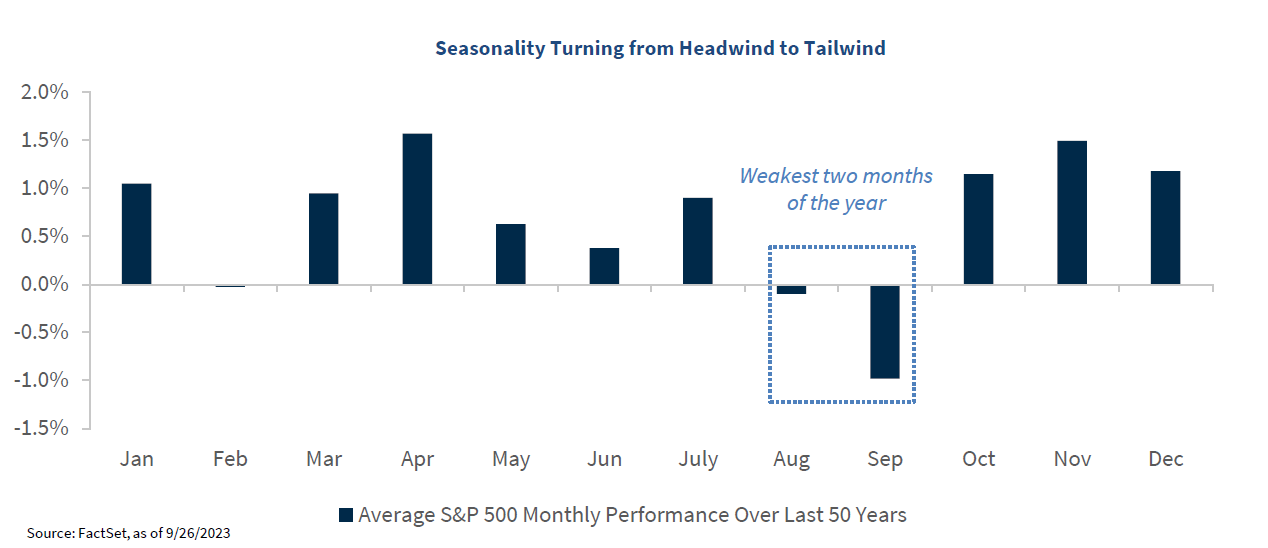

The third quarter of the year has brought some downside volatility with it. While it can be concerning when opening your statement, it is important to remember that minor pullbacks are very normal throughout the year. August and September are, historically, the toughest months on average for markets, as shown by the chart below. The good news is that the last quarter of the year tends to be one of the strongest on average.

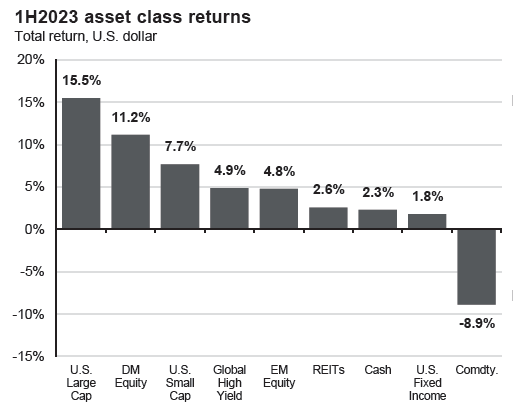

Over the past quarter, investor mood has shifted. The S&P 500 ended the quarter down 2.08%. A diversified portfolio ended the quarter down 2.63% if using a simple blended benchmark of (40% Barcap Aggregate Bond index, 40% S&P 500, and 20% MSCI EAFE International index). Quarters like this make it challenging to remember why you want to continue holding a diversified portfolio. Periods like that of 2000-2008 are a distant memory for most investors (and many have never experienced investing when U.S. markets and technology companies have struggled). If you dissect the returns of the S&P 500 year to date, you can see that most of the returns have come from the media dubbed “Magnificent Seven.” In reality, the remaining 493 companies in the S&P have contributed only about 2% of the positive 13% in year-to-date returns. The chart below shows how just these seven companies are responsible for most of the returns.

Source: Morningstar Direct

Maintaining a balanced approach to investing is important, as most of us are investing over a lifetime. While diversification may not always work over short periods of time, studies show it to be a successful strategy over the long term.

What contributed to volatility this quarter?

Higher intermediate and long-term interest rates have spelled trouble for equity valuations recently. The Federal Reserve (the Fed) did not raise rates in September but signaled that they are likely to raise one more time this year and are unlikely to cut rates in early 2024. This has caused longer-term bond rates to increase drastically over the summer (about 1%). We have continued to maintain our allocation to short-duration bonds, which has helped over that time period.

Higher interest rates contribute to equity volatility because investors view all asset classes through a risk/reward lens when determining where best to deploy money. When interest rates are low, investors are incentivized to reach for yield in equities as they pay an attractive dividend (more than treasury bonds were paying for a long time!). You also have the added upside potential of capital appreciation. When you can get interest above 5% in a money market or CD with extremely low risk, investors are less incentivized to invest money into equities, as most of the return needed to achieve long-term goals can be earned with little to no risk! Rates usually don’t stay elevated like this for very long. On average, the period between the last interest rate increase by the Fed and the first interest rate cut is nine months in historically similar periods. So don’t expect these high rates with no risk to stay around long.

Political brinksmanship is yet again holding the economy hostage to further both sides’ political agendas. The government averted a shutdown with only hours left but kicked the can down the road, so we may hear about this again in November. Like with the debt ceiling, we have been here before. The good news is, generally, shutdowns don’t coincide with recessions. There is a lot of noise and, usually, short-term volatility but not a longer-term impact on markets or the economy. The longest shutdown was 35 days at the end of 2018. While it created some temporary market fluctuation, it did not cause a larger economic issue. At that time, the economy contracted about .2% that quarter but got that back the following quarter because government employees get back pay once things open back up. Moody’s, the final of the big three debt ratings agencies to have the U.S. rated AAA, is questioning their AAA rating on U.S. government debt because of the behavior of the politicians.

Economic Growth is slowing

While Taylor Swift’s Eras Tour is coming to a close and noticeably adding to the local GDP of the cities she performs in, the rest of the economy might be better described by her song “Death By A Thousand Cuts.”

The consumer is out of extra money (one can only buy so many $90 concert t-shirts). The chart below shows how families had stockpiled excess earnings and government transfer payments from the COVID shutdown but have spent this excess savings over the past two years.

The UAW strike will continue to impact numbers like the above chart. As the strike expands, so does the risk of increased shutdowns and layoffs spread throughout the economy. It remains to be seen how long the strike will continue and, thus, how much of a negative impact on GDP it will have. While this strike will have economic consequences, it is only one industry. While there could be spillover if it goes on long enough (for example, people may go out to eat less if they are on strike and not earning their full wages), the UAW strike shouldn’t single-handedly be the cause of a recession.

Home affordability will continue to be hurt by high-interest rates.

Student loan payments restart in October, pulling more money out of the consumer’s pocket.

Jobs are strong, but job openings are pulling back.

These items, or something yet unknown, could be the tipping point for the economy to turn over into recession in early 2024. Most don’t realize we have already been in an earnings recession this year. This is classified as two or more quarters of contraction in earnings from the prior year. S&P 500 companies have experienced this as a whole this year. Equity markets are certainly spooked about this and are reacting accordingly now, even as the Fed tries to engineer a “soft landing.”

What is a soft landing?

In short, very rare. Ideally, the Fed will stifle GDP growth enough with higher rates to bring down inflation but not stifle so much that growth turns negative. Rather, it just slows down, avoiding a recession. They are counting on the strength of the labor market to remain, keeping the economy out of recession. Only time will tell if the Fed will need to keep rates higher for longer to put the inflation genie back in the bottle. They have come a long way in fighting inflation, as it was just a year ago that we were talking about 9% inflation, and now we are below 4%. The easy sources of inflation have been targeted and curbed (think supply chain shortages), so now it is time to let high interest rates work their magic throughout the economy.

Politics

The Speaker of the House, Kevin McCarthy, was ousted in a 216-210 vote, with 8 Republicans joining the unified Democratic vote. Patrick McHenry is serving as the temporary speaker, who is well respected in the house and should provide good leadership for now. Since we are well into the congressional term, proceeding without a formal leader shouldn’t be too disruptive to normal functioning as committees have already been formed and a rules process adopted. Electing a new speaker will, however, take valuable time away from working on funding the government past the November 17th deadline.

The media coverage is starting to pick up for the election in 2024. Undoubtedly, headlines will only pick up later this year and throughout next year. While there is no shortage of negative headlines during an election year, they tend to be positive for markets. Markets don’t care which party controls the white house. I think many view Republicans as being more pro-business and assume that returns will be far better than when a Democrat holds the office, but that isn’t true. The S&P 500 has gone up regardless of who holds the office most of the time. This is because markets focus far more on what is going on with the economy than on politics. American companies find ways to be innovative and successful regardless of who is leading the country.

While all of this noise can create market volatility, keeping your long-term goals in mind is more important than ever. We do not generate future forecasts; rather, we trust in the journey of financial planning and a disciplined investment strategy to get us through the more challenging times and stay the course. We appreciate the continued trust you place in us and look forward to serving your needs in the future.

Please don’t hesitate to contact us for any questions or conversations!

Angela Palacios, CFP®, AIF®, is a partner and Director of Investments at Center for Financial Planning, Inc.® She chairs The Center Investment Committee and pens a quarterly Investment Commentary.

Any opinions are those of the Angela Palacios, CFP®, AIF® and not necessarily those of Raymond James. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. There is no assurance any of the trends mentioned will continue or forecasts will occur. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. The MSCI EAFE (Europe, Australasia, and Far East) is a free float-adjusted market capitalization index that is designed to measure developed market equity performance, excluding the United States & Canada. The EAFE consists of the country indices of 22 developed nations. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. Diversification and asset allocation do not ensure a profit or protect against a loss. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Past performance is not a guarantee or a predictor of future results. Raymond James and its advisors do not offer tax or legal advice. You should discuss any tax or legal matters with the appropriate professional.