Contributed by: Angela Palacios, CFP®

We hit the ground running this year with a flurry of meetings with top notch investment managers. In January Angela Palacios attended the ETF.com conference where international investing was a hot topic. Angela shares some interesting insights along with notable quotes from some of our top money managers.

Ryan Barksdale of Vanguard: Due Diligence process

Melissa and Angela sat down with Ryan to discuss how Vanguard structures their investment committee in making key decisions as well as how they evaluate a company they are looking to bring on as a partner in making investment decisions. Ryan discussed with us their manager oversight and selection process. The keys in their investment selection process include low cost, top talent and patience.

Giorgio Caputo a portfolio manager and analyst at First Eagle

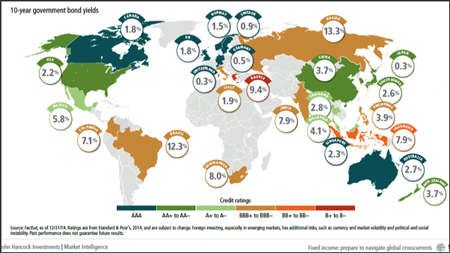

On the global front, First Eagle’s Giorgio Caputo noted that international valuations seem to be becoming more attractive relative to the US. And with global confidence at multi-year lows and depressed earnings, if anything goes right things would start to look attractive. US quality positions have been reaching their cash targets and they’ve been replaced with overseas holding. Caputo noted that their investors pay a tax by holding cash, high quality bonds, and golds in order to get lower risk as measured by volatility in the portfolios.

It was noteworthy that Caputo was meeting with us on January 23rd, which was the day that Mario Draghi announced new quantitative easing initiatives in Europe. Caputo mentioned that the trend has been to buy on rumor and sell on fact. This seemed to be repeated with the announcements.

Discussion turned to the global fears on deflation. Caputo noted the perplexing conundrum that worldwide labor pools are shrinking as populations age, but wage growth isn’t increasing with a tighter labor pool. He blamed this on a deflation pulse which is coming from the automation of equipment. Whereas a new factory 30 years ago might have employed 1,000 workers, today a similar factory might only employ 10 or 20 people with machines taking care of the rest.

Notable Quotes from some of our top managers shareholder letters

From Steven Romick President of FPA notes it has been rough weather for some time for deep-value investors. However, rather than letting the market’s and its price fluctuations drive them, they remain patient, picking companies that are easy to earn a return on for the price they are paying. They have to often sit in cash and wait for these opportunities as they are now, at least partially.

“Our money is invested alongside yours so we’re willing to look stupid for a time rather than act stupidly”

Rob Arnott Chairman and CEO of Research Affiliates notes that diversification in a bull market is always painful.

History and common sense suggest some serious caution going forward, given a potentially toxic brew of historically high valuation levels, peak earnings, an economic expansion that’s about to enter its seventh year, the markets’ evident addiction to monetary stimulus as the primary fuel for further rallies, and the stark divergence between U.S. stocks and pretty much everything else.

Angela Palacios, CFP® is the Portfolio Manager at Center for Financial Planning, Inc. Angela specializes in Investment and Macro economic research. She is a frequent contributor to Money Centered as well asinvestment updates at The Center.

This material is being provided for information purposes only and is not a complete description, nor is it a recommendation. Any opinions are those of Angela Palacios and not necessarily those of Raymond James. The information has been obtained from sources considered to be reliable, but Raymond James does not guarantee that the foregoing material is accurate or complete. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility. Raymond James is not affiliated with and does not endorse the opinions or services of Ryan Barksdale, Giogio Caputo, Steven Romick, Rob Arnott, or the companies they represent.