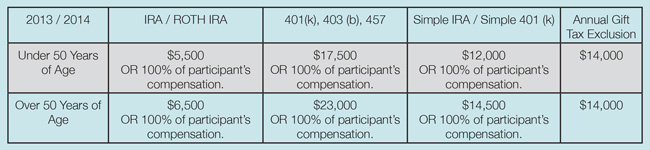

Here at The Center, we think of tax season as the most magical and exciting part of the year, but you might not see it that way. As you prepare to get your taxes in order, it is important to discuss some of the new laws going into effect for 2014 and to revisit some changes from 2013. Earlier this month, Matt Trujillo and Nick Defenthaler attended a portion of the University of Michigan tax seminar to brush up on the ever-changing landscape in the world of taxes. Below are a few key points that they felt may impact you:

Expiring Provisions in 2014

Deduction for expenses of elementary and secondary school teachers

Option to deduct state and local general sales taxes

Tax credit for energy efficient home goods (windows, doors, appliances, furnaces, etc.)

Don’t let home improvement sales people lead you to believe that the new product they are trying to sell you will generate a tax credit!

Elimination of private mortgage insurance (PMI) deduction

Consider checking a website such as Zillow or consult with a real estate agent to get an idea of what your home may now be worth. With the housing market improving, you may now have greater than 20% equity in your home. Consult with your lender to determine the best steps to eliminating your PMI.

Reminder of changes from 2013

In 2013, the Medicare tax changes went into effect for “high income earners” based on certain thresholds:

Single – Modified Adjusted Gross Income (MAGI) greater than $200,000

Married Filing Jointly – Modified Adjusted Gross Income (MAGI) greater than $250,000

This tax has two components, one based on wages earned above the thresholds and another based on net investment income above the thresholds.

0.9% additional Medicare tax on wages above thresholds

3.8% tax on the lesser of total net investment income or the amount of earnings above the thresholds (net investment income consists of dividends, interest, capital gains, rental income, etc. It does NOT include distributions from qualified retirement plans such as an IRA or 401k)

Ex. A married client’s MAGI for 2013 is $300,000. They also have $20,000 of net investment income. They are $50,000 over the $250,000 threshold. However, the $20,000 is less than the $50,000 overage; therefore, the 3.8% tax is based on the $20,000, resulting in an additional tax of $760 ($20,000 x 3.8%).

Affordable Care Act (Obamacare)

One of the biggest tax talking points for 2014 are the tax ramifications of the Affordable care act or “Obamacare”. A few key take-aways for 2014:

it's widely known that the penalty (in 2014) for not having insurance is the greater of $95 or 1% of income - this penalty will increase for the next several years to entice people to get health insurance.

For those individuals or families that are between 100% and 400% of the federal poverty level, you may qualify for a government subsidy to help offset your insurance premium costs.

In 2014 you will need to use a combination of last year’s earned income, and your projections of this year’s income to figure out whether or not you qualify.

If you find you are right on the cusp of qualifying for a subsidy, but are concerned about having to pay back the subsidy in full if you underestimate your income ... fear not! The rules regarding income are a “cliff”, meaning if you are wrong by $1 dollar you are subject to a penalty. However, the maximum penalty for 2014 is $400.

Example: Joe and Jane are 55 with no dependents. They estimate their income to be $62,000 and that qualifies them for a government subsidy. However, Joe gets an unexpected bonus at the end of 2014 and his income ends up being higher than 400% of the federal poverty level. In this scenario, Joe and Jane will be subject to a maximum $400 penalty.

Tax planning can be very confusing, especially since the IRS seems to change the tax code more often than electronics companies push new products. Please don’t hesitate to contact us if you have questions about your personal tax situation. Although we are not CPAs, we can still help to make your overall financial plan as tax efficient as possible and work together as a team with your tax professional to ensure we are all on the same page.

Nick Defenthaler, CFP® is a Support Associate at Center for Financial Planning, Inc. Nick currently assists Center planners and clients, and is a contributor to Money Centered and Center Connections.

Matthew Trujillo is a Registered Support Associate at Center for Financial Planning, Inc. Matt currently assists Center planners and clients, and is a contributor to Money Centered.

The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Center for Financial Planning, Inc. and not necessarily those of RJFS or Raymond James. Please note, changes in tax laws may occur at any time and could have substantial impact upon each person’s situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. All examples are hypothetical. Please consult the appropriate professional if you have questions about these examples and how they relate to your own financial situation. C14-002577