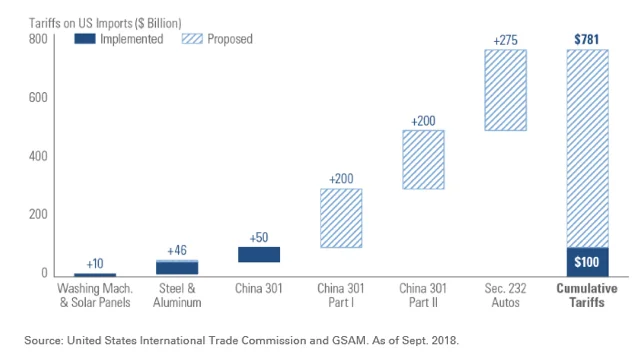

We don’t think this is how Trump foresees the end game. He hopes to force China to remove the tariffs they have historically imposed on our goods to put us on a level playing field of no tariffs, no subsidies and preventing intellectual property drain. Whether he is right and China will be forced to come to the negotiation table remains to be seen. Volatility should continue at slightly higher levels if this trade war continues to ramp up.

Politics

Mid-term elections are coming up, and that always puts politics at the top of everyone’s minds. There is also fear of impeachment that we often hear from clients and how that could affect portfolios. Impeachment is the process where the House of Representatives through a simple majority brings charges against a government official. After the government official is impeached, the process then moves to the Senate to try the accused. This must pass the Senate by a 2/3’s majority vote. If this happened, President Trump would be removed from the office, and the Vice President would take his place.

There is little to refer to in recent history to understand how markets would react here in the U.S. if this were to happen. Bill Clinton was impeached in 1998, and Richard Nixon resigned during the Impeachment proceedings but was never actually impeached. There have been recent unsuccessful attempts to impeach Donald Trump, George W. Bush, and, yes, even Barack Obama. When Bill Clinton was impeached markets were down in bear market territory (over 20% peak to trough on the S&P 500) for a short time before it rallied back. The Russian Ruble Crisis also occurred at the same time, so it is hard to say that the impact to markets was solely due to the impeachment process. So while President Trump likes to boast that the “Markets will crash and that everyone will be poor” if he were impeached that is likely not the case.

While we don’t think this has a high likelihood of happening, if it did, short-term volatility would probably occur while there is uncertainty and this is one of the many reasons why we maintain a diversified portfolio. If stocks retreated, it is likely that our bond portfolios would perform well and even a possibility that international investments would strengthen in the face of a weaker dollar. We believe a diversified portfolio with short-term needs set aside in cash or cash equivalents is one of the most effective solutions to an extremely rare event like this.

While this bull market may be getting old, it is important to remember they do not simply die of old age; rather they are killed by recessions.The yield curve is getting dangerously close to inverting but has not, thus not signaling a recession…yet.We are keeping a close eye on the yield curve and trade war as these items could quickly spill us over into a risk of recession. Markets can breeze along seemingly unconcerned by these types of risk until they aren’t.When sentiment swings from optimistic to pessimistic, it can happen almost overnight.As a result, we continue to maintain that having a diversified portfolio is extremely important.We are actively taking advantage of rebalancing opportunities to make sure your portfolios are prepared.If you have any questions or would like to speak with us more on these topics, please don’t hesitate to reach out to us!

Thank you for your continued trust!

On behalf of everyone here at The Center,

Angela Palacios, CFP®, AIF®

Director of Investments

Financial Advisor, RJFS

Contributed by: Kali Hassinger, CFP®

Contributed by: Kali Hassinger, CFP®